HOA insurance payouts often fall short because hidden damage, incomplete scope reviews, and weak documentation increase reconstruction costs after demolition begins. In this guide, we’ll explain how HOA boards, property managers, engineers, and reconstruction contractors can work together to strengthen insurance claims, uncover hidden damage early, and reduce costly funding gaps during large reconstruction projects.

Why HOA Reconstruction Claims Often Become Underfunded

A large HOA loss rarely unfolds the way board members expect. At first, the damage looks manageable. A few roof sections fail after a storm. Water shows up near windows. Residents start filing complaints. Then demolition begins, and the real problems surface. Saturated sheathing. Corroded framing. Balcony deterioration nobody knew existed six months earlier. That’s usually the moment reconstruction costs start climbing.

Across Texas, HOA boards regularly discover that the insurance settlement on the table will not fully cover the actual scope of work. And in many cases, the shortfall has nothing to do with the policy limit itself. It comes from weak documentation, incomplete scope reviews, missed code upgrades, or early adjuster estimates that never accounted for hidden damage behind the building envelope.

Knowing how to maximize HOA insurance payout for reconstruction means understanding how carriers evaluate risk, how engineers document failure, and how reconstruction contractors identify costs long before repairs begin. The associations that recover best financially tend to move early. They document aggressively. They bring in technical specialists before the claim starts narrowing. And frankly, that matters more now than it did a few years ago.

Texas reconstruction costs continue to rise. Labor shortages, ordinance and law coverage issues, material inflation, depreciation holdbacks, and stricter code requirements all create pressure during large multifamily claims. A first-pass insurance estimate often tells only part of the story. A lot of HOA boards don’t realize that until the project is already underway.

How to Maximize HOA Insurance Payout for Reconstruction

HOA insurance claims rarely become difficult because of obvious damage. Most disputes begin when hidden conditions appear after demolition starts. Water trapped behind cladding systems, deteriorated sheathing, corroded framing, failed waterproofing membranes, and code compliance upgrades frequently increase reconstruction costs well beyond the initial estimate. Insurance carriers look for documentation. HOA boards look for recovery. Those two goals do not always align.

A reconstruction claim becomes far stronger when the association treats the process like a technical investigation instead of a maintenance request. That means engineering evaluations, moisture testing, photographic records, contractor assessments, and detailed repair scopes all matter from day one.

Many associations lose money because they accept preliminary estimates prepared before the full site investigation takes place. Others fail to distinguish storm-related damage from long-term construction defects. In Texas, where hail, wind-driven rain, heat expansion, and waterproofing failures frequently overlap, that distinction matters.

Property managers who understand reconstruction often bring in experienced commercial reconstruction specialists before settlement discussions begin. That approach allows the HOA to validate repair costs, uncover hidden damage, and establish a defensible reconstruction scope before negotiations move forward.

Communities that delay this process frequently encounter underpaid claims, incomplete repairs, and special assessments that residents never expected.

Understand the Difference Between Replacement Cost and Actual Cash Value

One of the largest sources of confusion in HOA property insurance claims involves the difference between replacement cost value and actual cash value. Replacement cost coverage pays the amount necessary to rebuild damaged property using comparable materials and current labor pricing. Actual cash value, on the other hand, factors depreciation into the settlement. That distinction can dramatically affect reconstruction funding.

| Coverage Type | How It Works | Financial Impact |

| Replacement Cost Value (RCV) | Pays the current reconstruction cost | Higher reimbursement potential |

| Actual Cash Value (ACV) | Deducts depreciation from payout | Lower settlement amount |

Many HOA board members assume their insurance company automatically pays the full reconstruction cost. But older roofing systems, aging waterproofing assemblies, deteriorated siding, and deferred maintenance can trigger depreciation adjustments that reduce the payout significantly.

Here’s where things become complicated. Some insurance carriers release depreciation reimbursement only after reconstruction reaches completion. If the HOA lacks sufficient reserve funds or financing, the project can stall before full reimbursement arrives.

This can help explain why engineering documentation and contractor estimates matter so much during the early phase of the claim. Accurate reconstruction pricing supported by technical findings creates leverage during negotiations. Without it, associations may rely on generalized insurance estimating software that fails to reflect real-world reconstruction complexity.

Communities with extensive exterior damage often discover that labor shortages, code upgrades, difficult access conditions, and concealed deterioration increase costs substantially beyond the carrier’s original estimate. That gap usually becomes the HOA’s financial burden unless the claim receives proper support from the start.

Why Engineering Reports Often Determine the Size of an HOA Insurance Payout

Engineering reports tend to change the entire direction of a reconstruction claim. An adjuster may see surface-level damage. A forensic engineer usually sees something else entirely. Moisture migration behind cladding systems.

Structural movement around balcony connections. Failed waterproofing assemblies are hidden beneath finishes. The scope changes quickly once those conditions come into focus. And that’s often where disputes begin.

A lot of multifamily properties across Texas have older exterior systems that already carry years of exposure before a major weather event occurs. Hail or wind-driven rain may trigger the visible failure, but the underlying deterioration frequently extends much deeper into the wall assembly. Insurance carriers know this. Engineers know it too.

That’s why technical assessments matter so much during large HOA reconstruction claims. Without engineering documentation, many carriers rely heavily on adjuster estimates or Xactimate pricing models that may not fully capture concealed deterioration, code-triggered upgrades, difficult access conditions, or ordinance and law coverage requirements.

By the time demolition exposes substrate failure or hidden moisture intrusion, supplemental negotiations usually become unavoidable. Associations that bring in engineers early often place themselves in a much stronger position before settlement discussions begin. The report creates technical justification for the reconstruction scope instead of forcing the board to argue over opinions later.

According to the California Department of Insurance, the more information provided during a property loss investigation, the faster and more accurately a claim can be evaluated and settled.

Document Damage Like an Insurance Carrier Would

Insurance companies evaluate claims through documentation, not assumptions. That may sound obvious, yet many HOA boards still rely on casual photographs, incomplete maintenance records, or contractor summaries that lack technical detail. Comprehensive documentation usually includes:

| Documentation Type | Why It Matters |

| Engineering reports | Supports reconstruction scope |

| Moisture testing | Identifies hidden damage |

| Drone imagery | Captures roof and elevation conditions |

| Maintenance history | Establishes pre-loss conditions |

| Contractor estimates | Validates real reconstruction costs |

| Photo timelines | Demonstrates progression of damage |

Water intrusion claims create particular challenges because moisture often spreads beyond visible staining. A roof leak above a condominium unit may affect insulation, sheathing, framing, waterproofing membranes, and adjacent wall assemblies before interior symptoms appear.

Invasive testing frequently becomes necessary when the insurance carrier questions the extent of deterioration. Strategic openings inside cladding systems, balconies, wall cavities, or roofing assemblies can confirm whether hidden conditions exist.

Without that evidence, many insurance carriers classify the problem as isolated repair work rather than full reconstruction. That distinction can alter the claim value substantially.

Choose a Reconstruction Contractor Before Finalizing the Insurance Settlement

Many HOAs wait until after settlement approval before selecting a reconstruction contractor. That approach creates avoidable financial risk. HOA boards should also understand how to choose a reconstruction contractor for large Texas projects before settlement negotiations begin.

Insurance carriers typically prepare estimates using generalized pricing databases. Those estimates rarely account for the complexity of occupied multifamily reconstruction, staging logistics, access limitations, code upgrades, or concealed damage.

An experienced reconstruction contractor can identify missing scope items before the settlement becomes final. This is especially important for condominium communities, senior living centers, apartment complexes, and commercial properties where reconstruction affects residents, operations, and safety compliance simultaneously.

Communities that select contractors solely based on low pricing often face change orders later because the original estimate failed to include structural repairs, waterproofing replacement, drainage corrections, or code compliance upgrades.

That situation frequently creates tension between residents, board members, and property managers because supplemental costs emerge after work starts.

Experienced reconstruction firms approach insurance claims differently. They review engineering findings, evaluate hidden conditions, verify code requirements, and build comprehensive repair scopes designed around long-term building performance rather than cosmetic repairs alone. And that’s where many underpaid claims begin to change direction.

How Water Damage and Storm Claims Become Reconstruction Projects

Most large reconstruction claims don’t begin as large claims. A property manager notices staining near the ceiling after a storm. Residents complain about damp drywall around windows. Somebody spots cracking near a balcony edge during a routine inspection. On the surface, it looks isolated. Then the walls open up.

That’s when associations sometimes discover the moisture intrusion has been spreading behind the exterior assembly for months, occasionally years. Wet insulation. Deteriorated sheathing. Rusted connectors. Failed flashing details hidden behind stucco or siding systems. At that point, the conversation changes from repair work to reconstruction.

And this is where insurance disputes often become more technical. Carriers may classify portions of the damage as deferred maintenance rather than storm-related loss. Engineers may determine that the weather event accelerated a failure that already existed inside the building envelope. Reconstruction contractors may uncover conditions that the original adjuster estimated were never accounted for.

A condominium association dealing with hail damage, for example, might initially focus on roof replacement costs. But once demolition begins, moisture intrusion inside the wall cavity can trigger additional reconstruction requirements tied to framing, waterproofing membranes, ventilation systems, and current building code compliance. That kind of escalation happens more often than most HOA boards expect.

The Role of HOA Boards and Property Managers During Reconstruction Claims

Insurance claims often succeed or fail because of communication. Property managers, board members, reconstruction contractors, engineers, residents, and insurance adjusters all operate from different priorities. Unless the process remains organized, delays and disputes become inevitable.

Boards that maintain centralized records, consistent communication, and documented approvals generally move through reconstruction more efficiently. For occupied communities, reconstruction also affects resident relations. Noise complaints, temporary relocations, parking limitations, safety barriers, and schedule disruptions can create frustration quickly if communication remains inconsistent.

Strong property management teams often coordinate weekly updates, reconstruction schedules, resident notices, and contractor access procedures to minimize operational disruption throughout the project.

This becomes especially important for senior living centers, student housing properties, and multifamily condominium communities where resident safety and continuity remain critical throughout reconstruction.

How Texas Weather Risks Affect HOA Insurance Payouts

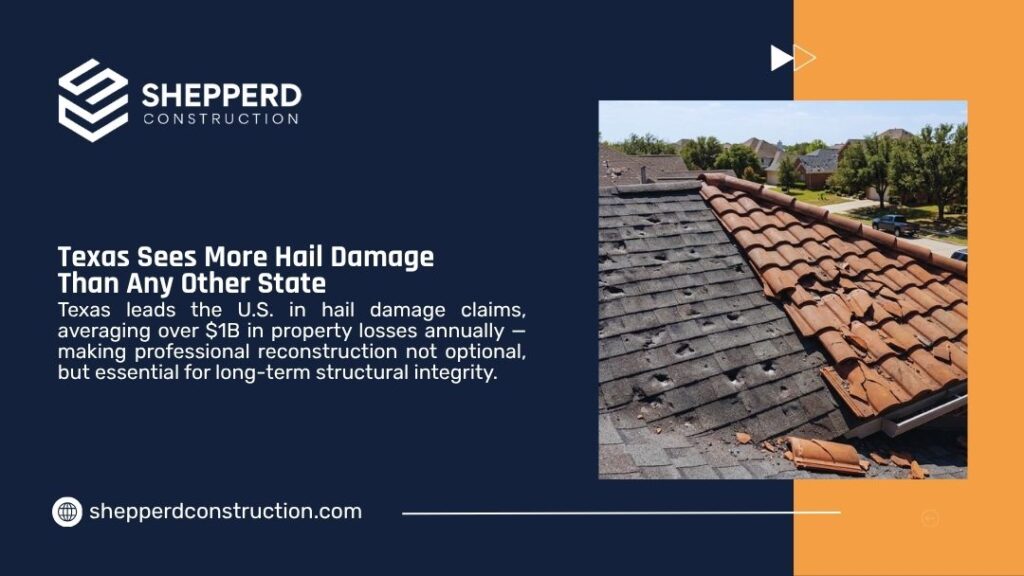

Texas reconstruction claims continue to grow more expensive each year. Texas faces some of the highest severe-storm exposure in the U.S. NOAA reports that from 1980–2024, Texas experienced 190 billion-dollar weather and climate disasters, including 126 severe storm events; in the most recent five-year period, the state averaged 13.6 billion-dollar events per year.

For insurance carriers, rising reconstruction costs create greater scrutiny during claim evaluation. Labor shortages, material inflation, permit requirements, and code compliance upgrades all increase settlement exposure. That means HOA boards must prepare stronger documentation than they did even five years ago.

| Texas Risk Factor | Reconstruction Impact |

| Hailstorms | Roofing and exterior cladding damage |

| Wind-driven rain | Moisture intrusion behind walls |

| Heat expansion | Waterproofing and sealant failure |

| Deferred maintenance | Reduced insurance leverage |

Older commercial and multifamily properties often require broader reconstruction than initially anticipated because modern building codes differ substantially from original construction standards. Insurance carriers may not voluntarily include those upgrade costs unless the association documents code requirements carefully.

Common Mistakes That Reduce HOA Insurance Payouts

Most underpaid reconstruction claims follow a familiar pattern. The board reports the damage quickly, but nobody orders a technical assessment. The insurance carrier prepares an initial adjuster estimate. Temporary repairs begin. Weeks pass. Then demolition exposes conditions that nobody included in the original scope review.

Now the HOA is chasing supplemental funding after reconstruction has already started. That scenario plays out constantly in large multifamily claims.

Some communities rely too heavily on the first insurance estimate without validating reconstruction pricing independently. Others delay engineering consultation because the visible damage appears minor at first. A few select contractors based strictly on low pricing, only to discover later that waterproofing systems, code upgrades, or concealed deterioration were never included in the bid.

And once residents start pushing for quick repairs, boards sometimes feel pressure to accept settlements before the full scope becomes clear. That creates problems later.

| Mistake | What Usually Happens |

| Weak documentation | Scope disputes develop |

| No engineering assessment | Hidden damage gets missed |

| Delayed reporting | Carriers challenge portions of the claim |

| Incomplete scope review | Reconstruction costs rise later |

| Low-cost contractor selection | Change orders increase |

| Ignoring depreciation holdback | Funding gaps appear |

The strongest claims usually involve early coordination between engineers, reconstruction contractors, property managers, and adjusters before settlement numbers become fixed.

What HOA Boards Should Do Immediately After Property Damage

The first several days after major property damage often shape the entire claim outcome. Associations should prioritize emergency mitigation, site stabilization, documentation, and engineering consultation before temporary repairs conceal important evidence.

Photographs should capture all elevations, roofing conditions, drainage areas, interior damage, and visible deterioration before cleanup begins. Maintenance records, reserve studies, and prior repair history should remain accessible because insurance carriers frequently review pre-loss conditions during investigation.

Large multifamily communities may also require moisture mapping, drone inspections, or invasive testing, depending on the severity of the event. Reconstruction contractors with multifamily experience often coordinate closely with engineers and property managers during this phase to establish realistic repair scopes early. That coordination frequently helps associations avoid scope disputes later in the process.

Why Long-Term Reconstruction Planning Protects Property Value

Insurance recovery represents only part of the larger issue. Communities that repeatedly defer exterior maintenance often experience higher insurance premiums, reduced property values, and greater reconstruction exposure over time.

Building envelope systems deteriorate gradually. Waterproofing assemblies weaken. Sealants fail. Drainage paths shift. Small vulnerabilities become larger structural concerns after years of weather exposure.

Forward-looking HOA boards increasingly treat reconstruction planning as asset preservation rather than emergency spending. Reserve studies, engineering evaluations, and preventative reconstruction projects can reduce future insurance disputes because the property remains in stronger condition before major storms occur.

That proactive approach also improves negotiating position with insurance carriers because maintenance history demonstrates responsible ownership rather than deferred care.

Questions HOA Boards Should Ask Before Accepting an Insurance Settlement

Before approving any settlement, HOA boards should evaluate whether the reconstruction scope fully addresses long-term building performance rather than visible cosmetic damage alone.

Questions surrounding hidden moisture, structural deterioration, waterproofing integrity, code compliance, and contractor pricing deserve careful review before reconstruction begins.

Associations should also verify whether engineering recommendations align with the settlement scope, reconstruction pricing reflects current market conditions, depreciation recovery remains available, temporary repairs concealed additional damage, reserve funding gaps still exist, and future code upgrades affect project cost. Communities that investigate these issues early usually reduce supplemental claim disputes later.

FAQs

What does HOA insurance usually cover?

Most HOA property insurance policies cover shared structures, exterior systems, common areas, roofing assemblies, and certain types of storm-related damage, depending on the type of coverage and policy exclusions.

Can an HOA negotiate an insurance payout?

Yes. HOAs frequently negotiate reconstruction scope, pricing, engineering findings, depreciation adjustments, and code-related upgrades during large commercial property claims.

Does HOA insurance cover the full reconstruction cost?

Not always. Coverage depends on policy language, depreciation, maintenance history, exclusions, code upgrade endorsements, and the accuracy of reconstruction documentation.

Why do engineering reports matter during reconstruction claims?

Engineering assessments help identify hidden structural damage, moisture intrusion, waterproofing failures, and code-related concerns that may increase reconstruction scope significantly.

Can deferred maintenance reduce an HOA insurance settlement?

Yes. Insurance carriers may argue that long-term deterioration contributed to the damage, which can reduce reimbursement or narrow reconstruction scope.

Reconstruction Claims Are Won Long Before Repairs Begin

Large HOA reconstruction claims rarely fail because of a single mistake. More often, problems build quietly in the background — incomplete scope reviews, hidden moisture damage, weak documentation, or early adjuster estimates that never captured the true reconstruction cost. By the time demolition exposes the full extent of deterioration, the financial gap has already started to grow.

That is why experienced HOA boards, property managers, and building owners bring reconstruction specialists into the process early. Engineering assessments, detailed scope reviews, and accurate reconstruction planning can make the difference between a fully supported insurance recovery and a project that leaves the community absorbing unexpected costs.For Texas communities in Austin, Dallas, Fort Worth, and San Antonio facing complex exterior damage, building envelope failures, storm-related deterioration, or large multifamily reconstruction projects, Shepperd Construction works alongside engineers, property managers, and ownership groups to help identify hidden issues, validate reconstruction scope, and support long-term property protection before repairs begin.