Right after a major Texas storm, the most expensive question often isn’t How bad is it? It’s a construction defect vs storm damage determination for insurance purposes, because that decision decides whether an insurer pays, partially pays, or walks away.

This guide lays out how carriers, forensic engineers, and attorneys sort causation, what policy language usually controls the outcome, and what documentation separates a paid claim from a denial.

Construction defect vs storm damage determination for insurance purposes

Construction defect vs storm damage determination for insurance purposes is a structured causation exercise, not a vibe check. The dispute boils down to a simple question with ugly consequences: Did the loss come from a sudden, covered event such as hail, wind, or wind-driven rain, or did it come from faulty construction, long-term deterioration, or a known weak spot that finally gave up?

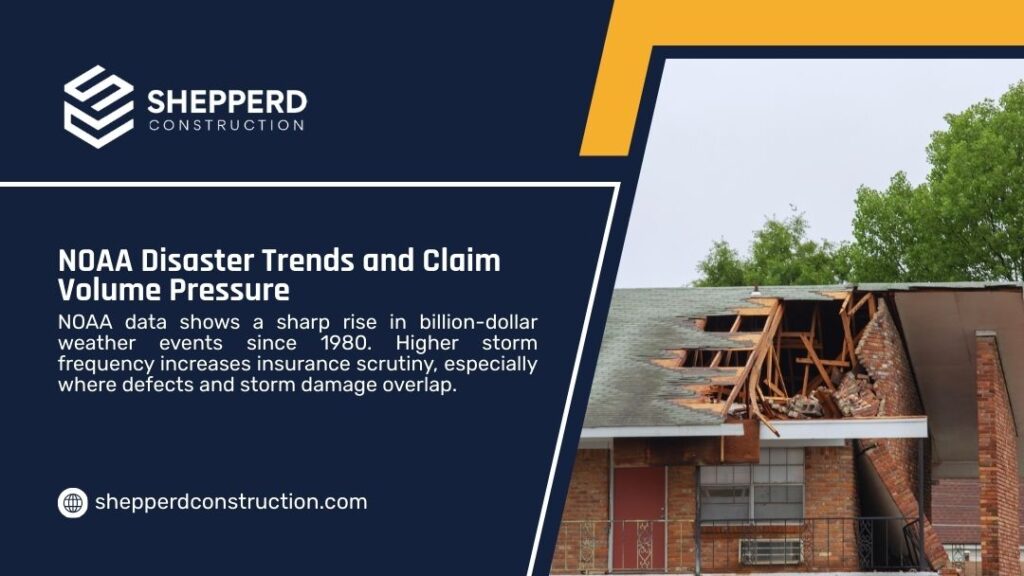

The tension has real fuel behind it. NOAA’s National Centers for Environmental Information shows the U.S. has faced hundreds of billion-dollar weather disasters since 1980, with the recent multi-year pace far above the long-term average.

That trend means more claims involving roofs, cladding, fenestration, and drainage, exactly the assemblies where small defects can masquerade as storm damage until the first big weather event.

Construction defect vs storm damage determination for insurance purposes usually hinges on three pillars: timing, mechanism, and policy wording. If the damage looks sudden but the failure mechanism points to chronic water migration, poor slope, missing flashing, or a bad install, the argument shifts fast from storm to defect.

That’s where construction defect claims begin, where insurance claims get contested, and where documentation becomes the whole ballgame.

After reviewing technical guidance and standard policy commentary, the storm vs defect fight rarely turns on one photograph. It turns on patterns, test results, and whether the file proves a covered peril caused distinct property damage, rather than merely exposing building defects insurance issues that existed for years.

Why does the distinction change insurance coverage outcomes

Construction defect vs storm damage determination for insurance purposes matters because the coverage path differs depending on the cause.

A typical property policy aims at covered losses from sudden events. Many policies contain exclusions for defective construction and faulty workmanship. In practical terms, insurers may accept that a storm occurred but still deny parts of the claim by arguing that the storm only revealed a pre-existing defect.

A widely cited explanation of the underlying policy framework on defective construction exclusions. Most property insurance policies contain some version of a ‘faulty workmanship’ exclusion.

That’s the axis of many poor workmanship insurance claim disputes. In construction defect vs storm damage determination for insurance purposes, carriers look for whether the claimed damage is the defective component itself, or separate ensuing damage caused by a covered peril after a defect exists.

The difference becomes sharp in scenarios like a window system that leaks during heavy rain. If the leak traces to missing end dams, poor sill pan detailing, or reverse-lapped WRB, the insurer may argue for excluded coverage due to the faulty workmanship exclusion language.

If wind creates a new breach, torn membrane, displaced flashing, or uplift that creates an opening, coverage arguments look different, even if the building had weaknesses.

This is also where construction defect insurance discussions enter the room. The property policy for the owner is one track. Liability insurance for the contractor is another track. In defect-heavy projects, attorneys often evaluate builders’ liability for defects and whether a contractor’s commercial general liability policy responds to unintended property damage beyond the defective work itself. The point is not academic; it changes who pays for demolition, drying, reconstruction, and long-term remediation.

How forensic engineers decide causation

Construction defect vs storm damage determination for insurance purposes rises or falls on causation evidence. In larger claims, multifamily, HOA, and commercial, the carrier often hires an engineer. The owner may do the same. When two engineers disagree, the claim turns into a documentation war with technical footnotes.

Forensic causation typically includes a mix of non-destructive and invasive steps. Moisture mapping can show distribution and migration paths. Selective openings can reveal missing flashing, improper overlaps, fastener patterns, sealant failure modes, and whether the assembly ever had a chance.

A federal technical resource from the Whole Building Design Guide (WBDG) frames the pattern problem plainly. Rather, most damage occurs because various building elements have limited wind resistance due to inadequate design, application, material deterioration, or roof system abuse.

That single sentence explains why the construction defect vs storm damage determination for insurance purposes becomes messy. Storms do real damage, no question. But weak assemblies fail at lower thresholds, and failure patterns can look stormy even when the root cause is faulty construction.

The engineer’s job is to answer: did the storm exceed design capacity, or did the assembly fail below it? Weather records, on-site findings, and construction history all matter. So do maintenance records. A roof with years of documented patching and interior staining will face a tougher path on storm causation than a roof with a clean history and a clear storm-correlated breach.

Typical indicators used in construction defect vs storm damage determination for insurance purposes

| Evaluation factor | Storm-driven indicator | Defect-driven indicator |

| Loss timing | Sudden onset that matches a documented event | Symptoms predate the event or appear gradually |

| Damage pattern | Randomized impacts, uplift zones, displaced components | Systemic failure at joints, seams, transitions |

| Water damage trace | New entry points with storm-created openings | Long-term migration behind cladding or WRB |

| Material condition | Fresh breaks, torn membranes, recent displacement | Chronic corrosion, rot, trapped moisture, delamination |

| Prior history | No repeat leaks, limited repair record | Multiple past repairs, recurring stains, and known weak spots |

| Mechanism of failure | Wind pressure, hail impact, debris breach | Poor slope, missing flashing, reverse laps, and wrong fasteners |

Construction defect vs storm damage determination for insurance purposes also depends on whether the claim seeks the cost to correct the defective work itself, or seeks repair for separate damage resulting from a covered peril.

Policy language that drives covered vs excluded

Even strong evidence can hit a wall if policy language is unfavorable. Construction defect vs storm damage determination for insurance purposes often turns on a few repeated clauses: exclusions for faulty construction, wear and tear, maintenance, and sometimes water intrusion limitations.

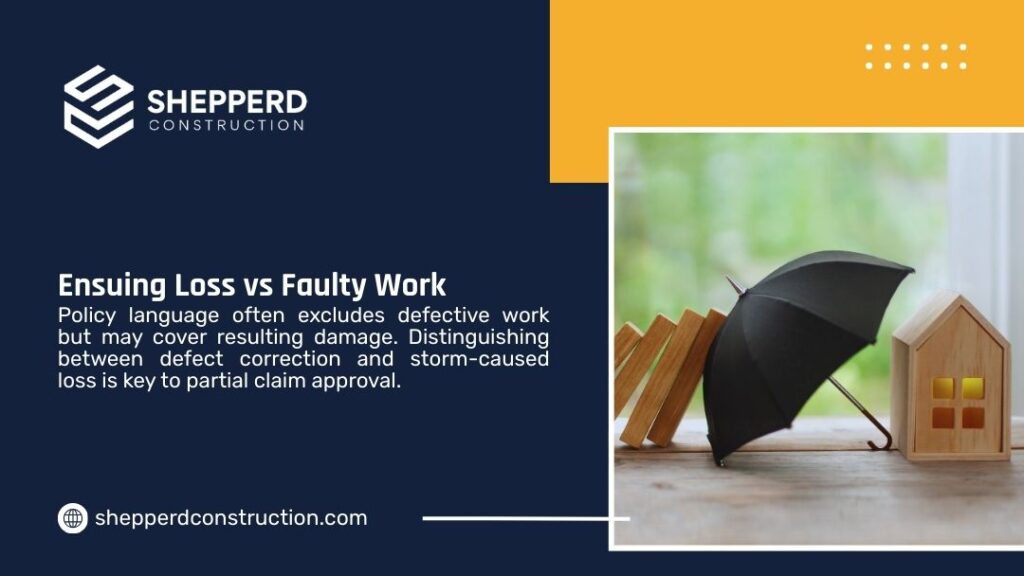

Many policies also contain an ensuing loss concept, where an excluded condition leads to a covered loss, and only the resulting covered portion applies. While homeowners’ insurance typically doesn’t cover poor workmanship, it may cover damage that’s caused by the work.

That’s the practical answer behind the common question: Is faulty workmanship covered by insurance? Often, the direct repair of defective work is excluded, while separate resulting damage may be considered, assuming it is not excluded elsewhere.

This is also where faulty workmanship vs negligence gets argued. Negligence is a liability concept; policy coverage is a contract concept. A contractor may be negligent and still have exclusions that limit coverage for repairing their own defective work. Conversely, a defect may not meet the legal standard for negligence but still give rise to a claim due to unintended property damage.

How policy types often intersect with construction defect vs storm damage determination for insurance purposes

| Policy type | What it commonly responds to | Common friction point |

| Property insurance | Sudden storm damage, direct physical loss | Defective construction and maintenance exclusions |

| Builder’s risk | Loss during construction | Defective design/workmanship limitations |

| Commercial general liability | Third-party property damage from an “occurrence.” | “Your work” and related exclusions; scope of damage |

| Professional liability | Design errors for architects/engineers | Usually not contractor workmanship |

When a claim turns on a construction defect vs. storm-damage determination for insurance purposes, the file should address the policy’s language early. Waiting until a denial arrives usually costs time, money, and leverage.

The concurrent-causation trap: when storms expose defects

Here’s the problem: storms often don’t create the weakness; they exploit it. A defective stucco termination detail may allow water entry during normal rain, but the owner never notices until wind-driven rain hits hard. The damage appears sudden, yet the assembly failure existed from day one.

Construction defect vs storm damage determination for insurance purposes becomes a question of proximate cause: did the storm create a new opening, or did it simply reveal a defect that already let water in?

This is why construction defect claims and storm claims can run side-by-side. Owners may pursue a storm claim under property insurance while preserving a construction defect claim against a contractor or developer, especially when the scope suggests systemic envelope failure rather than a localized storm breach.

In Texas multifamily settings, this shows up constantly in WRB laps, kickout flashing, balcony waterproofing, parapet caps, and window transitions. The storm is real. The defect is also real. The carrier may seek a clean exclusion path. The owner may seek a clean coverage path. The engineer sits in the middle with a flashlight and a core sample.

Documentation that wins the construction defect vs storm damage

In most contested insurance companies’ files, documentation does not help. It decides. The claim that survives scrutiny tends to have three layers: immediate event documentation, technical causation documentation, and repair scope documentation. The claim that collapses tends to have broad statements, sparse photos, and vague timelines.

Construction defect vs storm damage determination for insurance purposes benefits from storm-specific proof: date-stamped photos, weather verification, interior progression notes, and evidence of new openings.

It also benefits from defect-specific proof, but used carefully: prior repair logs can support a defect claim against a contractor, yet those same logs can weaken a storm claim if the carrier argues chronic conditions.

An evidence checklist that strengthens the construction defect vs storm damage

| Evidence type | Why it matters | What reviewers look for |

| Weather verification | Confirms a plausible covered peril | Local wind/hail/rain data near loss time |

| Pre-loss condition proof | Establishes baseline | Prior inspections, roof reports, clean interior photos |

| Post-loss photo set | Captures causation clues | New displacement, punctures, impact marks, uplift |

| Moisture mapping | Shows spread and pathways | Consistency with storm-created entry vs chronic migration |

| Selective openings | Reveals assembly conditions | Flashing, WRB laps, fasteners, substrate condition |

| Engineer narrative | Connects the mechanism to damage | Clear causation chain, not just observations |

| Repair scope detail | Separates covered vs excluded work | Line items tied to storm damage vs defect correction |

Construction defect vs storm damage determination for insurance purposes is also sensitive to what gets repaired too early. If a roof gets replaced before documentation, the most valuable evidence disappears, and the dispute becomes he-said-she-said.

Texas context: why this fight is common here

Texas sits at the crossroads of hail, straight-line winds, heavy rain, and fast construction cycles. That mix can amplify disputes over construction defects insurance and storm damage. On top of that, multifamily projects often rely on repeated details across hundreds of units. If one transition is wrong, it’s wrong everywhere, and the first big storm exposes it in bulk.

Meanwhile, hazard mitigation data shows why preventative steps matter. A National Institute of Building Sciences fact sheet on mitigation savings states federal mitigation grants ultimately save multiple dollars for every dollar spent, reflecting the economics of prevention over repair. This matters because owners who invest in envelope assessments and targeted retrofits before storms often reduce both property damage and claim disputes.

Construction defect vs storm damage determination for insurance purposes in Texas also tends to involve HOAs and property managers who must manage resident disruption, access, and communications, while trying not to compromise evidence.

Where reconstruction contractors fit into the causation story

Once causation becomes contested, the reconstruction plan can’t be casual. The scope must separate what is necessary to restore covered storm damage from what corrects underlying defects. In large properties, that split often requires close coordination among the owner, engineer, and contractor.

This is one reason many teams use specialized reconstruction contractors with experience in technically complex envelope work. If you need a contractor who understands reconstruction workflows and documentation expectations, Shepperd Construction presents its technical approach in its company background and details its service lines across core reconstruction offerings.

For HOA-driven projects where communication, coordination, and phased scheduling are essential, reconstruction contractors for HOA communities provide focused insight into community-based project requirements.

Construction defect vs storm damage determination for insurance purposes benefits from a contractor who can preserve evidence during openings, photograph assemblies properly, and scope repairs in a way that aligns with an engineering report, because insurers rarely pay for trust me estimates.

A realistic scenario: Multifamily water intrusion after a hail event

A Texas multifamily community reports widespread leaks after hail and wind-driven rain. The owner submits insurance claims that cite storm damage. The carrier inspects and argues that the true driver is faulty construction in stucco terminations and window transitions.

Selective openings reveal missing kickout flashing and reverse-lapped WRB at multiple elevations. Moisture mapping shows long-term migration behind the cladding, not a single storm-created entry point. The storm becomes the trigger, not the origin.

This is where construction defect vs storm damage determination for insurance purposes typically lands: the carrier may pay for discrete storm-created breaks while denying wholesale enclosure replacement as defect correction. The owner may then pursue construction defect claims against responsible parties, using the same forensic findings that limited the storm claim.

What to do when you suspect a mixed cause

Construction defect vs storm damage determination for insurance purposes gets easier when you treat the first week after discovery like evidence preservation, not repair season.

Start with disciplined documentation, then obtain an independent causation evaluation before major tear-off. If you need repair work urgently for safety, preserve samples and take thorough photos first. The goal is not drama; it’s clarity.

If you’re a property owner, attorney, engineer, or manager who needs to discuss a complex reconstruction scope with claim documentation in mind, Shepperd Construction is the direct path to a conversation about next steps.

Where this leaves property owners

Construction defect vs storm damage determination for insurance purposes is the hinge point for coverage, liability, and repair strategy. Storm events can create real, covered damage, but weak details and faulty workmanship often sit beneath the surface. Insurers focus on exclusions. Engineers focus on the mechanism. Attorneys focus on allocation and recovery paths. Owners just want the building to stop leaking and the financial bleeding to stop.

Treat causation as a technical problem, not a negotiation. Build a record that explains the failure mode, separates covered from excluded work, and ties scope to evidence. When the debate returns, because it will, construction defect vs storm damage determination for insurance purposes becomes something you can prove, not something you have to argue.

If you’re facing envelope or structural issues after a storm in Texas and the carrier starts leaning, don’t guess. Get the right forensic evaluation, preserve the right evidence, and align the reconstruction scope with the facts. That approach can help you protect coverage rights where coverage exists, and preserve defect recovery where it doesn’t.